Dossier

The economic situation of the forestry and timber industries in Germany

Susanne Iost | 24.07.2024

Official statistics on turnover, company and employment data provide insight on the economic sectors of forestry and timber. We quantify the value added in the forestry and timber industry and consider its development over time.

Timber balances comparing the volume of timber produced with its use have been calculated for Germany since 1950. The statistics are an important tool for recording the material flow of wood including imports and exports.

The cluster statistics for forestry and timber were developed to allow regular descriptions and evaluations of the socio-economic effects of the production, processing and treatment of wood. These statistics have provided annual data on the number of businesses and employees since 2000. They share important information on turnover and value added in the forestry industry and all economic sectors that are significantly dependent on the raw material wood.

The EU defines the economic sectors assigned to the cluster. The definition emerged from a tight raw material wood supply situation in the woodworking and wood processing industries. The aim was and is to ensure the added value of the companies in the forestry and timber sector. This applies in particular to rural areas because this also involves securing jobs.

Employment and companies are decreasing

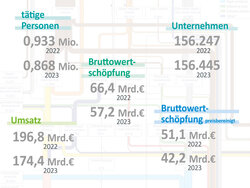

In 2000, more than 1.47 million people were self-employed or employed in more than 133,000 companies in the forestry and timber cluster. From 2009 to 2011, the number of employees hit just over one million. The global economic crisis has had a particularly significant impact on employment. In the following years from 2012 onwards, the situation is better again, but the number of employees shows a slight downward trend - in 2020, around 1.03 million people will still be working in the sector.

Businesses were less affected, their number even increasing slightly from 2009 to 2011. By 2018, however, the number of companies fell to 121,000. This downward trend appeared to continue in the following year. However, the decline from 2019 is largely due to the fact that the Federal Statistical Office's confidentiality guidelines took effect that year. In order not to violate the fiscal confidentiality regulations and prevent the drawing of conclusions about individual companies, no data was provided for the forestry industry sector service providers.

Turnover and gross value added show a positive trend since 2004

The total turnover of the forestry and timber cluster increased from 153.9 billion euros in 2004 to 187.7 billion in 2018. Gross value added increased from just under 50 billion euros to 58.65 billion euros over the same period.

In the course of this increase, there are short-term reductions in both key figures; the year 2009 is particularly striking here. As a result of the global economic crisis, sales were then at 161.5 billion euros, while gross value added is at 51.1 billion euros. The drought-related forest damage is reflected in declines in turnover in 2019 and 2020. Gross value added also falls slightly in 2019 compared to 2018, but rises again in 2020 to 58.1 billion euros.

In the course of achieving global climate protection targets, the contribution from the cluster to climate protection is increasingly important. CO2 is stored in the long term in durable wood products, such as furniture or construction wood. In addition, greenhouse gas emissions can be avoided if wood-based raw materials are used instead of fossil resources.

The cluster statistics for forestry and timber are an important source of information for businesses and professional associations, and serve as a basis for political decision-making. One example is a subsidy program launched in 2021 to support companies affected by the drought-related forest damage of recent years. Data from the cluster statistics are used to estimate the amount of funding required.

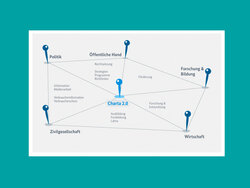

In 2002, the German government set a goal to increase wood use in Germany by 20 percent over ten years. This target was laid down in the "Charter for Wood". Also, in the Charter for Wood, it was stipulated that the wood used should be sustainably produced. In this case, the term "sustainable" means that the use of wood creates jobs and added value, especially in rural areas. Cluster statistics have established themselves as the most important measuring instrument in order to be able to assess whether these goals have been and are being achieved. The first "Charter for Wood" process, 2004 to 2014, successfully increased per capita wood consumption from 1.1 to 1.4 cubic meters of raw wood.

The second Charter for Wood (2.0) is closely related to international and national policy strategies such as the Climate Protection Plan 2050 and the national bioeconomy strategy. In addition to the sustainable use of wood and the assurance of value creation and employment in the forestry and timber cluster, the goals are now also the qualitative growth of the forestry and timber industry and climate protection. Concrete fields of action are timber construction, wood-based bioeconomy, efficient use of raw materials and materials, forest management, value creation and employment, communication with stakeholders and research.

Recently, it has often been discussed whether the printing and publishing industry should still be considered part of the forestry and timber cluster. Especially in the publishing industry, the importance of digital processes and products is increasing. Thus, only a part of the publishing industry is still dependent on wood as a raw material.

Parallel to the digitalization of many areas of life and the economy, ways are currently being sought to replace fossil raw materials with more sustainable bio-based raw materials. For example, wood is increasingly being used to produce basic chemicals, plastics and textiles.

Thus, the importance of wood as a raw material in economic sectors is changing as our economy modernizes. These changes will be reflected in future cluster statistics.